Loans meant for education normally enable students to tide over the gap between college costs and their ability to pay for the financial assistance and after scholarships they benefited from during their college time.

These loans are obviously good because they help the students to achieve their education goals. The decision by students to take loans can be very difficult because they will have a huge impact on their lives for quite a number of years.

It means that students must make smart choices when it comes to borrowing so as to figure out how their lives will shape out in future with their loan burdens in tow.

Eighteen year-old students will therefore have to visualize today the realities of their tomorrow when thinking about these loans so as to avoid unnecessary problems in future.

As much as these loans are helpful, students and their parents should be careful and concerned when it comes to determining the cost of college fee loans.

This begs the question: when do we say that students’ loan debts are too much? Do the overall costs outweigh the resultant academic and professional benefits?

Student Loans: How much is too much

The right amount of student borrowing is tied to the goals, the risks of the borrower and their future lifestyle post-graduation.

Perfect worlds would be looking at average students’ loans of $0 since college would be free of charge. In the real world though, an individual has to make an informed decision on the amount they borrow accordingly to avoid sinking deeper in debt post college.

The rule that guides college borrowing is that you should borrow less than what you will earn post college.

In the event that your student debt at graduation is less than your yearly starting salary, then you ought to be able to settle the loan in ten years or thereabouts.

If not so, you might struggle to make payments; a situation that will force you to extend your repayment period. In order to avoid over borrowing, you can do the calculations on the monthly payments to see the correlation between your future budgets in relation to the loan payment.

In a nutshell, the job you will get after college will be a determinant on how easy or hard it will be to repay the loan.

Another way to avoid over borrowing is by making comparisons of colleges using the net price which is calculated by getting the difference between the total college cost and the gift aid.

When done with this analytic comparison, you will be able to know which college in your preferences offers a better deal.

You also need to borrow what you need but not as much as you can and so, do not borrow excess to pay for secondary comforts, vacations or expenses which are not school related.

Just live a student’s life while in school so that after graduation you do not live like a student. It is not that students’ loans are evil, no. The thing is that most students borrow a lot more than what they need and as such they are not prepared on what and how much they will pay after they graduate.

With the latest statistics and patterns, it is apparent that students’ loans will burden them way after they graduate.

Statistics from the US federal reserve indicate that Americans are less burdened by credit card debt compared to students’ loan debt.

The credit card debt in the US is about $925billion compared to $1.75trillion in students’ loan debt. Parents also bear a huge burden in terms of repaying student loans.

About 3.7million parents have borrowed approximately $05billion from the federal government to facilitate their children’ education. Statistics from the class of 2020 indicate that about 54 percent of students in college borrowed and later graduated with a debt of around $28,000.

The average loan debt for students summed up to about $41904 from both the federal and private colleges in which the average monthly amount repaid by the students stood at roughly $460.

An average borrower can take about twenty years to settle an academic loan debt since an average loan can accrue an interest of up to $26000 in a period of twenty years.

Students must therefore avoid getting into too much debt by sticking to a number of thumb principles.

First, the sum borrowing for undergraduate studies must be limited and guided by their expectations on what they will make after their first post-graduation. To make this easier, they can find books on statistics that illustrate starting salaries, projected needs and intended growth.

Secondly, payment should not be more than 8-10 percent of their anticipated total monthly income. Manageable debt to income ratio will help in comfortably paying the loans.

If the beginning salary is around $37000 per annum, about $3100 per month, a monthly loan payment of 9 percent should be around $236.

If these two are put into consideration it will be easy to meet their repayment duties while at the same time guaranteeing a good return on college investment.

Is 40,000 in Student Loans a lot?

The cardinal rule about a student’s debt is that it should be not more than the salary you will receive in your first job after graduating. $40000 is just as fine and not much as long as your job prospects after graduation will guarantee more than per year after you have graduated.

When borrowing, the money is purely meant for school fees, and you are expected to have a proper budget for it in terms of tuition, books and other academic-related programs.

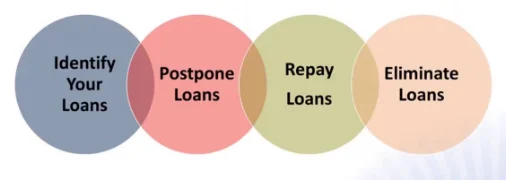

How to Manage your Students Loan

1. Know your Total Debt

You need to have a clear picture of the amount of money you owe. Students graduate with either federal or private sponsored loans having organized for fresh financing in each of their years in school.

Therefore, knowledge of their total debt can help a lot in payment, consolidation or even waiver.

2. Understand the Grace Period

Loans do have grace periods for repayment and students’ loans are not an exception. A grace period is the time given after graduation before one starts to pay back their loans.

These periods will differ from college to college with a range of six to twelve months’ grace period before payment.

3. Paying Automatically

Additionally, you might consider borrowing federal students’ loans since they have low interest rates with very flexible repayment terms. As you do this, also sign up for auto pay so that your student loan remittance will be sent to the lender directly from your bank account.

This reduces your chances of being caught late with payment and at the same time you might as well enjoy other incentives.

4. Deferring payment

One might be caught up in a situation where employment is hard to come by. In this case asking your student loan lender to defer payment would be a smart option.

In case you have the federal students’ loan and qualify for loan deferment, you may not be charged any interest during that period. Also, seek information on loan forgiveness that can boost you as well.

Should you not qualify for deferment, applying for forbearance to stop paying the loan temporarily can help though interest accrued during this period will be included in the principal amount of the loan.

Parents and students need to have an in-depth discussion on how to finance college fees by looking at the interest rates, repayment terms and flexibility.

More importantly, should take note and interest in unsubsidized federal loans because their interests only accrue when the students are still in college.